Mitigating 280(e) Disallowance in Your Cannabis Company With a Brand IP Entity

A cannabis operation is just another small business – with added complexity, of course. Not only do cultivators and manufacturers manage a high-value product tied to strict regulations, but also all the other processes associated with running a small business: employee scheduling, vendor relationships, sales, marketing, and cost management.

Many costs related to running a cannabis business are stable and somewhat predictable. Your sales, direct cost of goods sold (COGS), and overhead – utilities, rent, depreciation, and equipment – will all show on your P&L statement as fixed costs.

The new Cannabis Brand Entity (CBE) you set up will also act as the sales and marketing arm of your business

For cannabis businesses seeking to save money, that leaves you with sales and marketing expenses. What are some ways you can make those line items work for your business, instead of against your profit margin? Sales and marketing costs can eat 5-10%+ of your revenue if you aren’t careful. For a $10MM company, that’s close to $1MM in expenses that you cannot roll into a cost of goods sold deduction.

There is a big opportunity to unlock those deductions – while still staying on the right side of 280E guidance. Here’s one solution cannabis operators can explore to make their marketing expenses work for their business model.

Setting Up a Cannabis IP Entity

The basic concept we’re going to take you through is the process of setting up a separate entity that owns your intellectual property. This IP ranges from trademarks, images, and slogans to trade secrets, recipes, techniques, and formulations.

The new Cannabis Brand Entity (CBE) you set up will also act as the sales and marketing arm of your business. This CBE is not subject to 280E restrictions; it does not traffic in a Schedule 1 controlled substance. Your cannabis operation will pay a reasonable royalty to this brand entity, a royalty that can be rolled into COGS adjustments.

Of course, the process is slightly more complex than this summary suggests. We’ll break down the nuances as much as possible to give you context as to how this arrangement works. We strongly recommend working with a cannabis tax expert to understand if this option will work for your specific cannabis operation.

How the Funds Flow in a CBE

In this scenario, we’ll use the example of a cannabis manufacturing business; however, these same principles would also apply to a cannabis cultivation business.

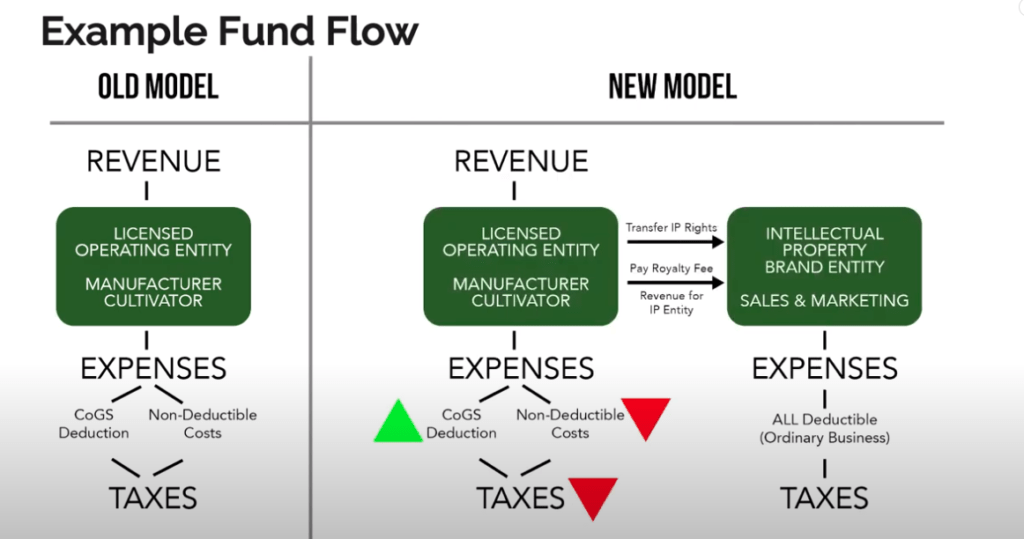

First, let’s look at the fund flow illustrating how money moves in the existing business model. This will give as a starting point with which to compare our new business model that we are suggesting you establish for tax purposes.

From the image above, in the initial fund flow on the left side, the operating entity, has a manufacturing license, generates revenue, has expenses, and pays its tax bill every year.

Now on the right, you see the updated fund flow where we have two entities; The manufacturing entity and the IP company. The manufacturing company has transferred ownership of all its IP to the IP Company. In return, the manufacturing has licensed use of that IP, paying a reasonable royalty to the IP company in return.

It is important to note here that the IP company is a fully separate business entity with its own revenue streams, expenses, accounting books, employees, and more.

Tax Implications for Licensing Your Cannabis IP

What does this mean for manufacturing business (and the IP entity) from a tax standpoint?

For the manufacturing entity, they will pay a royalty once per month to the IP entity. This payment will be fully taxable income for the IP entity.

The IP entity will also have sales and marketing expenses associated to offset that income. Essentially, the IP entity performs all of the sales and marketing functions that the manufacturing business used to handle in-house. The manufacturing business will license IP to make products, and the IP company does all of the sales and marketing of those products.

Now the manufacturing business also needs to know how to allocate and deduct that royalty payment.

There is a lot at stake here: you must properly categorize your payment to see any tax savings. If you get this wrong, you could be paying a 30% tax rate on a $1.2MM royalty payment, equal to $360,000. Get this right, and you will save that $360k on your tax return.

The main pillar is to focus this royalty payment on the manufacturing procedure. Remember, the intellectual property that you are licensing includes trade secrets, recipes, techniques, and formulations. Without these IP assets, you couldn’t make your product. It is critical that you have well-documented SOPs that become your techniques and trade secrets.

Sec. 1.471 is most applicable and where we get our guidance. Yes, this tax code is pretty broad, but it does bring up that “indirect production costs” are inventoriable costs and we will get more clarity of WHAT those costs are by looking at another tax code, Section 263A also known as UniCap.

So in Section 263, there is a list of non-exclusive indirect costs that must be capitalized and those include manufacturing procedures and special recipes. And your royalty can be added to CoGS as long as it is a manufacturing procedure or special recipe that is necessary or directly benefiting the production or resale of the product.

Understand that you must use a GAAP accrual accounting adjustment to move costs from inventory to CoGS.

What Royalty Payment Structure Should You Use?

With this high-level understanding of the tax implications and the position you would take, the next question to answer is the payment structure and amount of the royalty payment.

There are two benchmarks that we will use to triangulate the amount you should pay in royalties: market rates and your financial projections. Remember, this has to be a reasonable royalty based on data – not an arbitrary number you pull from thin air.

First, determine your total projected sales and marketing costs from your existing, original cannabis manufacturing business. Let’s say for this example the manufacturing company is projected to generate $20MM in annual revenue, and their sales and marketing expenses will be $1.2MM per year.

In the end, the IP company will be taking over all of these sales and marketing functions, so those will be going to be the IP company’s expenses. This royalty is considered revenue to the IP company: to fully ‘unlock’ that $1.2MM from 280E and taxes, you have to make sure the IP company has that amount of expenses to offset the revenue. $1.2MM is the threshold we are trying to hit as far as spending on business activities at the IP entity.

Now the next step is to take a step back and look at the market. What is considered a reasonable royalty for marketing in the cannabis industry?

When you look at enough royalty agreements, you will see that there is typically a minimum payment and then some percentage of sales. Therefore, in this scenario, the IP company would set a minimum annual royalty payment of $500k, $750k, or maybe even $1MM so that you know that at least that amount is going to be deductible every year.

The reason for a minimum is because until you scale up to that $20MM in annual revenue, you can’t charge a 30% royalty on those lower-end sales numbers. That percentage doesn’t fit the contract norms.

Next, you need to look at the royalty payment in terms of a percentage of sales. Once you scale up to $20MM, what percent of revenue will the IP entity charge the manufacturing business?

In the cannabis industry, there are not many public market numbers or contracts available for you to refer to in creating a model. Typically, in other lines of business, you see royalty rates from 1-5% of sales; but cannabis businesses could be higher, maybe up to 8-10%. We suggest consulting a tax and contract expert to make sure you’re making a safe estimate.

In this scenario, if you had a $1MM minimum royalty payment up until the manufacturing company generates $20MM in sales, you would then switch over to a percentage of revenue. It would likely be safe to charge 5% of revenue as the royalty payment going forward.

What are the Risks of This 280E Tax Strategy?

It’s hard to say what the risk level of this setup will be, as there has not been a tax case yet testing this relationship in the cannabis industry. This is not the same type of cannabis management company set up that we witnessed failing in the Alternative Health Care Advocates case. As this is a pure royalty position, we believe the risk profile is lower.

Let’s review three ways to reduce your exposure:

- Set the royalty rate at a reasonable amount. You can’t set it at 30-35% of sales because no one in any industry does that. Have the minimum fee and set a reasonable percentage and make sure that you have a very tight, well-thought-out royalty agreement contract written by an experienced lawyer. Also, look at the total royalty rate at an annual rate. If you set a minimum payment of $500,000 and the manufacturing business only makes $2.5MM in revenue, that’s a 20% royalty…that’s probably too big.

- Keep the manufacturing and IP businesses as separate legal entities. These businesses must have separate books, separate accounting, separate business plans, no commingling of funds – which means having separate bank accounts– and no consolidated tax returns. You could have the same ownership percentages, but consider changing officers or managing members. Don’t have any workers be employed by both companies.

- Have well-written standard operating procedures. Delineate clearly what qualifies as your intellectual property. These SOPs will become your trade secrets, formulations, and techniques that are licensed out. Consider filing for patents and trademarks to establish more evidence that these are, in fact, protected pieces of property.

A last word on why having bullet-proof SOPs is important. If you want to expand your operation to other states, then licensing out your IP is how you scale up. These arrangements strengthen the validity of your position with your IP entity. In your home state, you may own both the manufacturing and licensing company. But in other states, if you have a relationship with a different manufacturer, then you can set up a licensing and royalty agreement with them to produce using your trade secrets. If the IRS questions your position, you can point out that you have this same type of IP arrangement with a second or third cannabis manufacturing company in Nevada or in Michigan.

If you own a cannabis manufacturing or cultivation business, then you should consider implementing this strategy to save on your taxes.

Please reach out to us today to learn more about the process and get started.